The Bank of Canada came out with their rate announcement this morning & have kept rates unchanged, shocker! To put this in context the Bank has stated they will not look to raise rates until 2023. That’s what they’re saying. What could change that?

Well, remember that little thing by the name of inflation that for the last year I’ve saying is one of the more important factors to watch? It’s picking up. Commodities have been on a tear, housing is soaring & we’ve certainly noticed an increase in our monthly bills. Fixed rates, which are based on the government of Canada bond yields, have increased significantly in the last 2 weeks. The bond market generally does a good job at front running the economy & things, for now, are better than expected.

Keep in mind there is a great incentive in the powers that be talking down inflation while it slowly creeps up on everything b/c it allows debt to be inflated away as that debt becomes worth less. That’s known as a soft default. You’re not NOT paying your bills, your paying back bills that aren’t worth as much. The risk in talking down doing that is if all of a sudden the market realizes this they could be a sharp increase & shock which could end up being recessionary.

The Bank highlighted inflation is at the lower bound of its 1-3% range & expects it to move to the top end in the next few months but sees that slowing down as the excess capacity in the economy exerts downward pressure. Will they make it to 2023? I have no idea but will be watching it closely.

Thanks for watching & have a great day.

https://ZupanMortgage.com/wp-content/uploads/2020/05/Citywide-logo.png00adminhttps://ZupanMortgage.com/wp-content/uploads/2020/05/Citywide-logo.pngadmin2021-03-10 10:08:242021-03-10 10:08:41Bank of Canada Rate Announcement March – no change!

The Bank of Canada kept rates unchanged today in their scheduled rate announcement. The economic rebound in Canada has been better than expected but as we now face a second wave, much of the current outlook is dependent on how covid plays out here at home. Housing has been strong. Personally I’ve seen a lot of clients migrating from the downtown core to places like Victoria, the interior & further out in the lower mainland. Working from home is something many are taking advantage of by upgrading for space.

Of course these record low mortgages rates are a big reason for housing’s strength so how does the interest rate forecast look currently? Officially, the Bank of Canada has said they don’t expect to be raising rates until after 2022. They want to hit a 2% inflation target before moving to any increases & they expect inflation to start to pick up slowly early next year.

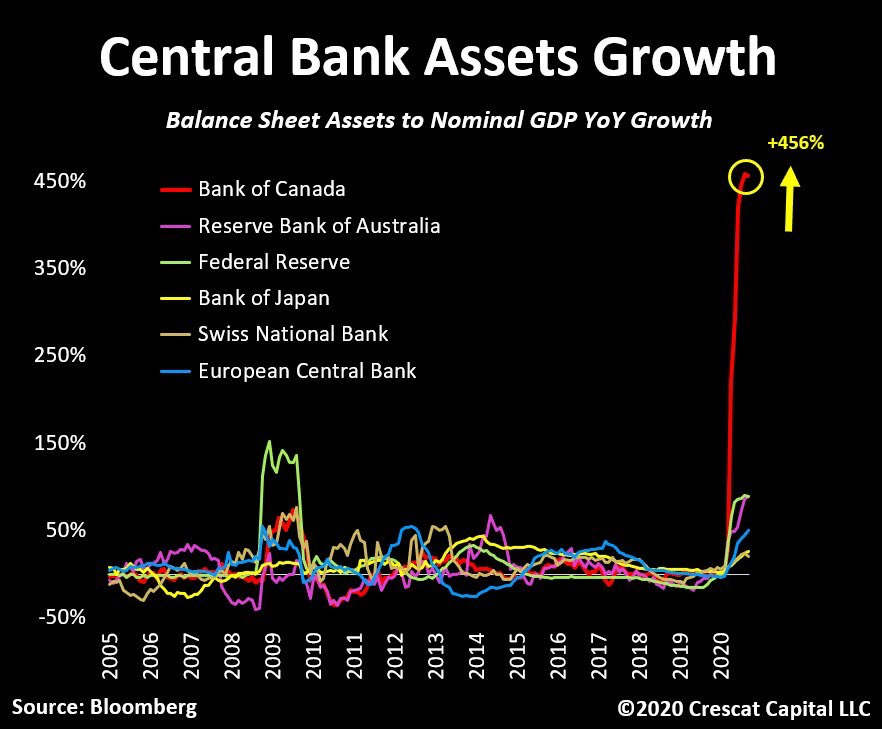

The Bank is also continuing its bond purchase program, which suppresses yields (and interest rates). I wanted to include this chart as it really illustrates the eye popping balance sheet growth of Canada’s central bank compared to others around the world since the pandemic started.

Currently our central bank owns 1/3 of our federal debt… so we’re generating debt then buying our own debt. Yes this is something many central banks are doing globally, but as soon as inflation expectations pick up, that means more bond buying is required (so more increases to the balance sheet) in order to keep interest rates from rising. It can turn into a vicious cycle where the end result does not fare well for our currency & the cost of goods.

I don’t think we’ll see much of a change in outlook until the end of this year but we have one more rate announcement coming up in December so will update you then.

That’s it for me today. Thanks for watching & have a lovely Wednesday.

https://ZupanMortgage.com/wp-content/uploads/2020/05/Citywide-logo.png00adminhttps://ZupanMortgage.com/wp-content/uploads/2020/05/Citywide-logo.pngadmin2020-10-28 10:36:262020-10-28 10:36:38Bank of Canada Rate Announcement October- no change!

Good morning! This morning our new Bank of Canada governor, Tiff Macklem, carried through with his pledge in July to keep rates at this level for at least 2 years & left rates unchanged at this morning’s policy announcement. Central banks around the world seem committed to letting inflation run hot by keeping rates low. Let’s not forget that low rates has most certainly NOT created meaningful inflation for the last few decades, so what would be different about this time around?

Following 2008 the massive amount of money supply creation (which pales in comparison to what we’ve seen in the last 6 months), went almost exclusively into propping up financial assets. What’s different this time around is a commitment to the fiscal side & putting money into the hands of the ppl & the economy, not just wall street. Governments are creating debts, then printing money to pay for those debts. What could go wrong?

On a recent CNBC interview one of the greatest & most successful investors of the last few decades, Stan Druckenmiller, came out saying for the 1st time in a long time that he is actually worried about inflation & that we could easily see 5-10% inflation in the coming years. Ironically, he also pointed out the rising risks also going the other way towards deflation, as every period of deflation is preceded by an asset bubble. With companies are soaring 30%, 40%, 50% on news of stock splits (which add zero value to a company), when bankrupt companies are seeing their stock prices double while their bonds are trading at a few cents on the dollar, when sports bloggers like Dave Portnoy are calling Warren Buffet washed up while they tout the mantra of stocks only go up, it’s hard to argue we are in anything but a mania driven bubble.

So we have 2 risks – deflation & inflation. What does that mean for your mortgage?

Fixed rates are incredibly low right now. You can lock in rates at or under 2% for the 1st time in Canada’s history. Could mortgage rates go lower? Yes. Could they go negative? No. Are we already very close to zero? Yes!

Now on the flipside to that, could inflation impact the central bank’s commitment to keeping rates low? Yes! Could we see a major breakout of rates from this multi decade downtrend towards zero? Yes! Historically have inflation breakouts taken shape quicker than most expect? YES!

The way I see it, mortgage rates are incredibly attractive right now. They could go a bit lower, but they could also go A LOT higher. What impact would having a mortgage rate that’s 0.5% lower have on your life? What about a rate that’s 2% higher?

These are some of the questions I’m having with clients right now & if you’d like some help mapping through these scenarios, please get in touch.

I’m Ryan. Thanks for watching. Have a great day.

https://ZupanMortgage.com/wp-content/uploads/2020/05/Citywide-logo.png00adminhttps://ZupanMortgage.com/wp-content/uploads/2020/05/Citywide-logo.pngadmin2020-09-09 09:06:202020-09-09 09:20:29Bank of Canada Rate Announcement – no change!

Good morning, the Bank of Canada kept rates unchanged this morning with their scheduled rate announcement. From the Bank’s release, the severe impact of Covid appears to have peaked & the gargantuan policy response has helped replace lost income & cushion the effect of the shutdowns. Right now the Bank’s forecast is for a sharp, partial rebound followed by a slower grind back to pre-crisis levels. The grind part of that being the key element.

Let’s

remember that policy response was more life support than it was

stimulus. Debt, which was already at high levels pre-covid, is giving

up future consumption for greater consumption today. Unless that debt

is used to create a new income stream that will help pay for that new

debt, then it creates a drag on future cash flows. If I take out a

mortgage to buy a vacation property, then those payments are going to

take away from what I can spend my money on & invest with

otherwise. If I use that financing to buy a rental property, I can

acquire that asset without my monthly consumption being as impacted.

The economic gravity of what has happened in Canada & around the

world the past few months is something that will weigh on us for a long

time.

What

can you do? If you’re able, use this as an opportunity. Take

advantage of low rates by creating another income stream, or by reducing

your current debt load. If neither of those are options & you are

one of the millions turned upside down from has been the worst financial

event in anyone’s memory, think about what you can do moving forward to

help keep you brace for the unexpected.

I

was thinking last night how, through most of my life, it has felt like

we have been on a linear path of progress & of course, life is not

linear. Life is cycles of booms & busts, bright times followed by

dark times. Winston Churchill said never let a good crisis go to

waste. Find a way to emerge from this stronger than you were before.

If that means taking government help, education, a career change, using

technology to improve productivity, re evaluating your monthly

budgeting, investing, spending more time with loved ones, find a way to

use this situation as a learning experience. It is clear we have

entered a darker time as humans. Crisis’s happen & are happening

more often than ever in our lifetime. Find a way to better brace for

the unexpected.

I’m Ryan, glad to be clean shaven again & to have a reason to iron my dress shirts. I hope you have a great day.

This has been a bit of a moving target & we will do our best to keep this as up to date as possible, but below is a list of the best ways to contact your lender regarding payment relief. PLEASE get in touch if you are having any issues getting through or questions related to the relief available.

Also, make sure to clarify with your lender the financial & credit repercussions of payment deferral.

I’ve been getting a lot of questions about how the coronavirus will impact mortgage rates so wanted to get this out there to cover what those looking to buy a home, or have mortgages coming up for renewal, or are thinking of maybe refinancing, should expect. A lot of people you know have mortgages & are going to benefit from watching this so please forward on to friends or family or whoever you think is going to want to know what’s going on.

I’ll try to keep this simple: LOWER RATES. Until the world has gotten this virus under control there will be no pressure on rates to go up. The Bank of Canada dropped rates by twice their usual 0.25% cuts last week, something they haven’t done since the great financial crisis, and that was just as this virus was entering Canada. Is that the last of them? No. Bond yields, which are what fixed rates are priced on, have been finding new bottoms, I expect us to see rates follow suit & continue to hit new all time lows.

Regardless of your personal thoughts on Covid19, what is very clear is how contagious this is. Forget death rate & how many ppl die compared to the seasonal flu. What this boils down to is the potential of exponential growth.

Consider this example: if the number of people in a stadium doubles every day, and it takes 50 days for the entire stadium to be filled, how many days does it take before half the stadium is filled? The answer is 49. On day 48 = 25% full. On day 47 = 12.5% full. On day 46 it’s 6.25% full. So in the span of 4 days we go from 6.25% full to 100% full. That gives you an idea of how quickly things can get out of hand & why authorities want to act early.

The path I think we can expect are schools shutting down, employers allowing people to work from home, conferences & sporting events being cancelled. The countries that have gotten a handle on this thing have done so by implementing draconian measures of more or less locking people inside their homes to prevent the spread & that is where I think things are likely to head. To frame all this from the perspective of the economy, it’s not good. Canada’s growth had already been slowing BEFORE corona had shown up. Look at commodity prices. Look at the price of oil right now. That decline started before the Saudi / Russia feud.

Think about the knock on effects of what happens when people aren’t going out for dinner, going to the mall, taking trips, booking flights. When companies aren’t making sales, they cut costs through layoffs. When people don’t have jobs, they don’t spend money. You can see how a deflationary shock like this can be self reflexive. All of this points to rates continuing to drop.

What does this mean to you? Looking purely from the mortgage perspective, this is obviously good. If you have a mortgage that is over 3%, get in touch because in the last week we have found a ton of opportunities for clients to save money refinancing their mortgage. I still think it’s a bit early, but we’re at least knowing these opportunities exist & waiting for the timing to be optimal before finalizing anything.

If your mortgage is coming up for renewal in the next 6 months, DO NOT take your lender’s early renewal offer. At least, not without checking in with me. I have yet to see one in the last few months that is attractive enough to make moving early worth it but I can at least promise to shoot you straight & can tell you quite quickly what you should do.

If you’re looking to buy a place, as always, be patient. There is going to be opportunity out there & on the mortgage front, you’re going to be looking at rates we have never seen in Canada’s history.

The final piece I want to add here is that there is already a ton of government debt in the system & we’re going to see a lot more. The way governments are going to eventually get out of this debt burden is by trying to create meaningful inflation. Any of us who have spoken to our parents about mortgage rates in the early 80s & 90s, have heard of rates in the high teens & even above 20%. We got there because the government was trying to reel in inflation. I’m not saying we’re going to go to 15%, but even rates going from the mid 2% to the mid 5% is going to create a shock to a lot of borrowers. There is a lot you can do in advance of that to prepare.

Once this worm has

turned, it is going to be essential for you to have your mortgage not

with a bank specialist, not with your account manager at the branch,

neither of those avenues get compensated to service

their existing book of business. It is very rare for your banker to

approach you with a refinance opportunity.

That is really where us brokers are worth our weight in gold. That’s how we make money is by finding these opportunities & saving you money. You want to work with someone who has your best interests at heart, who knows what’s going on & knows when to do things so you can time it appropriately.

The last thing I’ll add, if you are concerned with the risk of inflation, not in the near term, but down the road, get in touch. I have some awesome strategies for that, one in particular the “inflation hedge,” which I would love to share with any who are interested.

Thanks for watching & have a great day!

https://ZupanMortgage.com/wp-content/uploads/2020/05/Citywide-logo.png00adminhttps://ZupanMortgage.com/wp-content/uploads/2020/05/Citywide-logo.pngadmin2020-03-12 14:24:522020-03-12 14:24:56What Impact Will Coronavirus Have On Mortgage Rates?

What a week we’ve had… Yesterday the US Fed did something they hadn’t done since oct 2008. Oct 2008, for some reason that time period stands out but I can’t quite put my finger on why, OH YA, Lehman Brothers went belly up & the global financial system was in shambles!

So

what did the Fed do? The Fed had a scheduled meeting for 2 weeks from

now but decided to do an emergency rate cut of not 0.25% but 0.5%.

Fast

forward to this morning & the Bank of Canada matched them with the

same 0.5% drop. This was the first time Canada has done such a move

since spring 2009. Not very encouraging precedents…

The

reason for the big move was due to the corona virus. Regardless of

whether you think this is overblown hype or a legitimate concern, the

reality is covid19 brought China’s economy to its knees. China consumes

about half of the world’s resources so that alone poses a problem for a

commodity based nation like ours.

But

what can Central Banks really do to interest rates that are going to

counter that? They’re not buying oil. They’re not buying plane

tickets. Earlier in the week we saw the Bank of Japan step in with 500

BILLION yen in liquidity injections, followed by the Bank of Australia

cutting rates, but both their respective markets, just like the US, rose

briefly then fell. What we are seeing is Central Banks losing their ability to actually impact markets & growth.

So

what happens from here? Is this big move the only we’ll see? If

you’ve been following these summaries of mine then you’ll know that I’ve

been expecting lower rates since the summer. The US has a dollar

shortage & strength problem they’re trying to fix. You’ve got the

eurozone on the brink. I think this is going to be a race to the

bottom. And all that was before coronavirus.

I’ve

been following this virus since mid January & it was pretty clear

even back then that this is an incredibly contagious virus. Anyone who

looks at how exponential growth works can see how quickly this can

overwhelm a country’s resources, particularly healthcare, & that, to

me, is the big risk here at home. Call me a fear monger or buying into

the hype, or whatever… a country like China doesn’t completely shut

down if it wasn’t absolutely necessary.

So

in summary, big rate drop today. Bond yields are either at or near all

time lows. The loonie is weak. Business investment is down. It’s not a

pretty sight & it appears this could just be the beginning.

How’s that for a happy morning update? I’m Ryan, thanks for watching & have a great day.

https://ZupanMortgage.com/wp-content/uploads/2020/05/Citywide-logo.png00adminhttps://ZupanMortgage.com/wp-content/uploads/2020/05/Citywide-logo.pngadmin2020-03-04 09:59:002020-03-04 10:40:25Big Move By the Bank of Canada

https://ZupanMortgage.com/wp-content/uploads/2020/05/Citywide-logo.png00adminhttps://ZupanMortgage.com/wp-content/uploads/2020/05/Citywide-logo.pngadmin2019-09-16 11:17:072019-09-16 11:17:11August Real Estate Stats Show Pickup in Activity

The federal budget came out yesterday & there were some minor actions targeted to first time buyers I wanted to highlight.

First off, don’t get excited. The impact in Vancouver is likely going to be limited, but basically the gov’t is increasing the home buyers plan RRSP withdrawn from $25k to $35k, effective immediately. Note that the funds still need to be repaid in the same 15 year window.

The second incentive is from CMHC which will provide 5% of a first time buyer’s down payment on a resale property & 10% on a new build. The buyer still needs at least 5% down, but this will help reduce borrowers mortgages to lower their payments.

The loan is interest free so from that perspective, why not take it. Lower payments, less interest. The funds will be repaid upon the sale of the home, but so far it is unclear how this would work exactly. CMHC might share in the capital gain or loss, receiving a portion of the sale price, but we will wait to see how this will be rolled out exactly.

There are requirements to meet this program, namely:

-household income under $120k

-borrowers must have the min 5% down

-the purchase price cannot exceed 4 times the buyers household income.

Based on this, the effective limit on purchases will be less than $500k so the impact of this is going to be limited in our market.

While the budget does allocate $10billion over 9 years for new rental homes, it does not bring in any tax breaks or reduced red tape to developers, which, in my view is a more productive & efficient way to attack these issues, but, hey, I’m not running the country!

https://ZupanMortgage.com/wp-content/uploads/2020/05/Citywide-logo.png00adminhttps://ZupanMortgage.com/wp-content/uploads/2020/05/Citywide-logo.pngadmin2019-03-19 19:37:072019-03-19 19:41:25Housing Highlights From Federal Budget 2019

Effective Jan 1 the newest mortgage rule was put into effect in Canada – the “stress test.” This video is going to give some background on mortgage stress tests, then explain the new rule.

Currently, if a borrower is buying with less than 20% down payment & is therefore getting an insured mortgage, they already have to qualify off of a stress test rate (being the 5 year posted rate, currently at 4.99%). For borrowers with 20%+ down, they can avoid this same stress test ONLY if they take a 5 year fixed mortgage (or longer), which means that if they want a variable or, say, a 2 year fixed, they would have to qualify off the 5 year posted rate not their actual interest rate.

The new requirement specifically impacts borrowers getting uninsured mortgages, which you can think of as borrowers with 20% down or more. Now, they will have to qualify for their financing based off a new stress test being their interest rate + 2%. So if they chose, say, a 5 year fixed mortgage with a rate of 3%, they would have to qualify based off a rate of 5%.

The irony of all this is that shorter terms generally mean lower rates, which therefore means that borrowers will qualify for larger mortgages taking shorter terms & shorter terms result in a borrower being more vulnerable to interest rate increases which doesn’t exactly benefit clients.

If you’ve bought a presale prior to these new rules being implemented & are curious how this will impact you, as long as you have a purchase contract dated prior to Jan 1, 2018, you’ll be grandfathered under the previous rules.

Additionally, you have a mortgage coming up for renewal & are not able to qualify to switch under the new rules, all is not lost. There are ways we can still qualify you off the previous rules.

If you’re looking to buy a place but can’t qualify for the price point you need under the new rules, give me a call. There are a still a few ways we can still get you into a purchase qualifying of your contract rate.

Ryan Zupan

604.250.6122

ryan@citywidemortgage.ca

https://ZupanMortgage.com/wp-content/uploads/2020/05/Citywide-logo.png00adminhttps://ZupanMortgage.com/wp-content/uploads/2020/05/Citywide-logo.pngadmin2018-02-01 16:00:512018-02-01 16:00:51What is the new mortgage stress test in Canada?